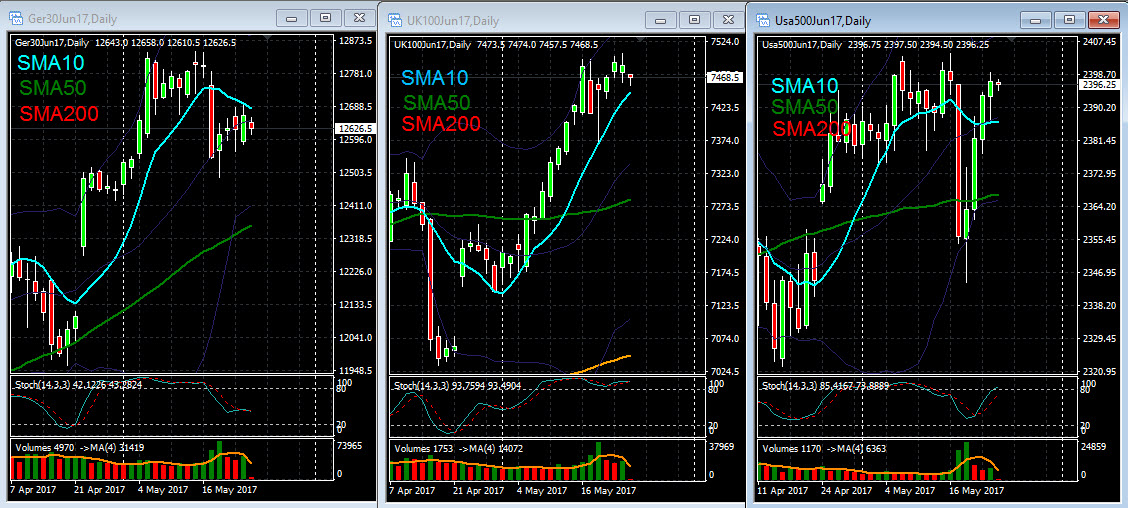

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

In the pre-opening, the European markets traded with light losses. Affecting the opening was the behavior of Asian markets that extended their losses, after the rating agency Moody’s reduced Chinese long-term debt ratings. Consequently, the stock market fell and the Chinese currency, the Yuan, depreciated. In this context, the European companies most exposed to the economy of the country will now attract the attention of investors. On the other hand, in the business scope, Antofagasta, Glencore and Marks & Spencer will now disclose their quarterly accounts. The behavior of the oil price and the disclosure of the minutes of the Fed will be part of the essential points for today.

Despite fears of another terrorist attack, this time in Manchester (UK), investors have been somewhat optimistic about the presentation of the State Budget to congressmen. The market ended yesterday’s session on positive territory, with the S & P500 index supported mainly by the financial sector. In the last 14 sessions, the Nasdaq has been valued 12 times. The focus has been on the presentation of the State Budget, which includes cuts in areas such as health care or food programs, with the goal of stabilizing federal spending around 3600 M.USD over the next 10 years . On the other hand, one of Donald Trump’s objectives also refers to the sale of half of the US oil reserves, in addition to the agreement signed by Trump in Riyadh, to supply Saudi Arabia with military equipment worth 110 M.USD . In terms of economic indicators, sales of new homes fell in April from 11.40% to 569 000, a drop more than expected. For today, the minutes of the last Fed meeting are expected to be published. Until last week, more or less veiled, the Central Bank admitted that the prospects for implementing the economic policies of the Trump Presidency (tax cuts, more flexible regulation, Infrastructure plan, etc.) justified the rise in interest rates in 2017. At a time when the OPEC meeting is expected to take place tomorrow (tomorrow), the weekly oil inventories will be known today Of the Department of Energy.

The Asian squares ended the session on mixed terrain. Moody’s downgraded China’s debt rating from “Aa3” to “A1”, predicting that authorities would approve more economic stimulus. However, the agency has shifted China’s “negative” outlook to “stable”, since at “A1” level, “risks are balanced”, highlighting the country’s mechanisms to halt financial instability. Despite expecting Chinese GDP to continue to grow, Moody’s ensures that the country’s growth will slow in the coming years.