Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

Stocks enter Tuesday’s trading with trepidation after suffering the worst losses of the year on Monday. Today will mark the day of the repayment of Greece to the IMF and the end of the EU support program / IMF / ECB to this country (23h00 GMT, the deadline for Greece to repay the 1600 M. € due to the IMF). Non-payment is not technically a default. The default would only materialize if Greece fails to repay the ECB in the near term (July 20). The latest countries that have failed a payment to the IMF were Zimbabwe, Cuba and Sudan. Today also ends support program that had been extended in February in order to provide time to the Greek authorities drew up a plan of action. As agreement was not reached during this period was not demobilized the last tranche totaling 7200 M €. Despite the heavy losses suffered by European equity markets during yesterday’s session, this retreat was somewhat peaceful not having seen a spiral of rampant sales. In relative terms, the European indices only lost the gains that had been achieved last week. In the bond market, the pattern is similar. The yields of the countries of southern Europe rose but only a portion of what had retreated last week. More serious was the reaction of the Greek stocks. While the Athens stock exchange has been closed, on Wall Street an ETF on Greek shares lost 19.44%. This resilience of European assets will be put to the test today when the Italian Treasury auction 7000 M € in debt maturing in 2020 and 2025. The Greek situation raises several questions. One of these issues, more related to the equity markets, is to what degree the current uncertain environment affects the preference of global managers for European equities. Since the beginning of the year, the European indices have been the beloved of global investors due to more attractive key ratios compared to other geographical areas, the positive outlook for the European economy, to lower interest rates against the US, the weakness of the euro and above all the ECB’s repurchase program. The validity of these factors still persists, the big question is whether it can overshadow the unpredictable risk of the Greek crisis. In the coming days, investors will monitor developments in relation to Sunday’s referendum. Even in this field, the positions of Athens and Brussels differ. According to the Greek Government, this referendum aims only to establish the position of the Greek people against the tax plan of measures by the ECB / IMF / EU, while for the European authorities is a real referendum on the permanence of Greece in the eurozone. According to sources, the Greek Prime Minister rejected last night, a final offer made by the President of the European Commission.

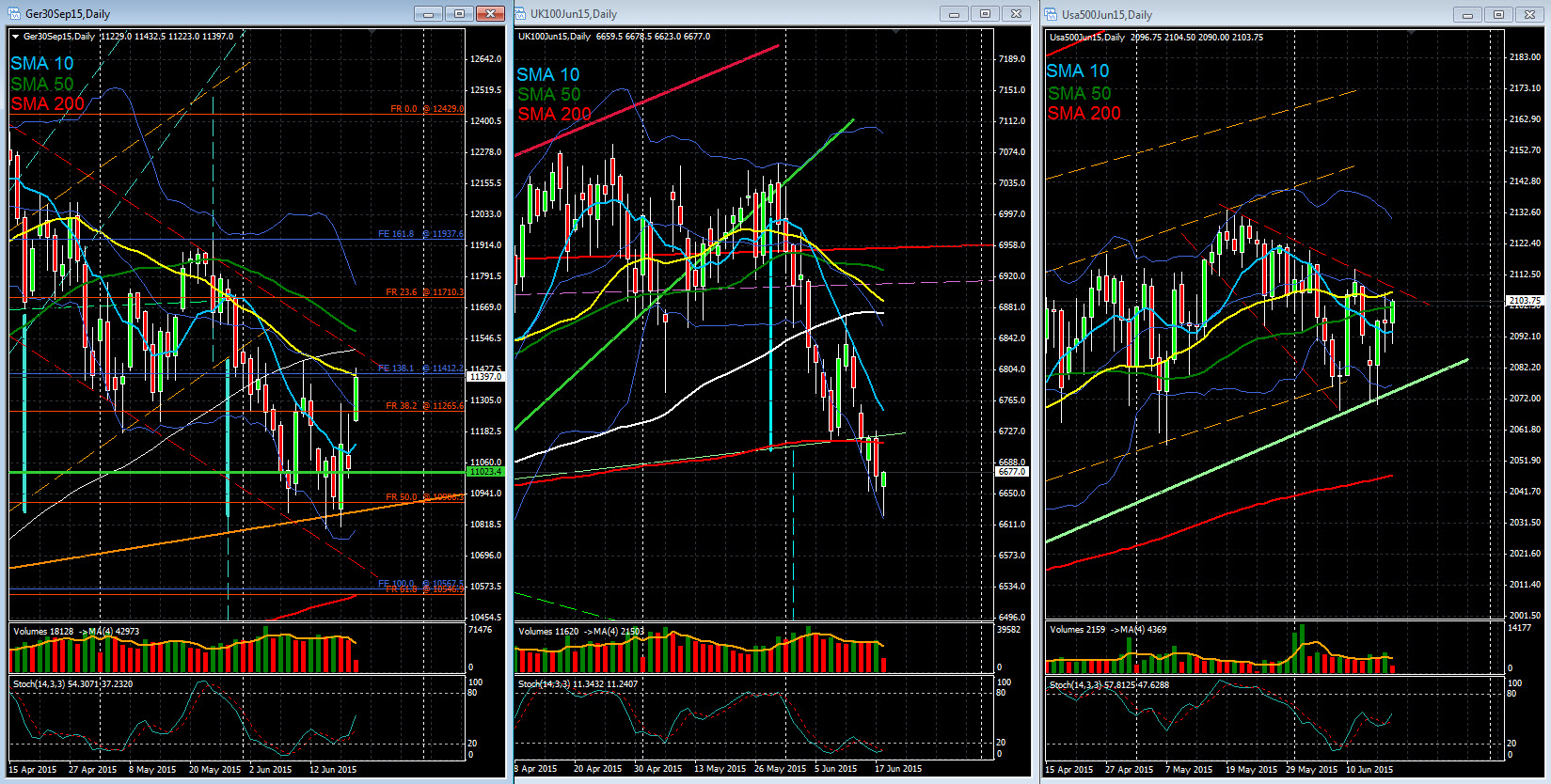

US markets closed with very wide losses. The reaction of US investors was significant. Until yesterday, and as at similar times in the past, the US stock markets have always considered the Greek situation a European issue with limited potential to affect the US economy. However, given the high uncertainty that is spreading throughout the Eurozone, US investors fear that the modest European economic recovery is compromised, adversely influencing this quarter the attempted acceleration of the US economy. In a risk aversion context, the publication of economic data has been relegated to a lower plane. Technically, yesterday’s session is an important warning. Since late March, the S & P had fluctuated between 2067 and 2135, not showing any clear trend in the short term. Yesterday, the S & P broke the lower part of this range and may signal the beginning of a descending phase. This signal can be thwarted if the S & P back to close within that range.